- Positive Skew

- Posts

- Should You Buy the Dip After Taking Profit?

Should You Buy the Dip After Taking Profit?

A portfolio-centric approach to reduce pain and increase gains

Jay Jenkins

July 13, 2024

You caught a heater. Maybe you bought ETHE before the SEC approval. Maybe you were early to BILLY or WIF. Maybe you’ve HODL’d bitcoin for years and you’re finally ready to take some profit off the table.

So you sell, and with pockets full of cash you have some decisions to make. What do you do? What’s the next play?

You could:

Pay off your mortgage?

Buy some stocks or an ETF?

Reload on high beta shitcoins?

Or maybe its time to fire up the private jet and take off for a tax-haven in the tropics?

With so many choices, you’ve got to think ahead. Plan a little. You need a system.

This is mine.

Crypto Portfolio Management 101

Portfolio management is how you deal with risk. It’s being intentional about diversification, taking profit, and allocating your capital.

Risk is a real, tangible thing (especially in crypto). Things can go wrong, prices will go down, and you can quickly lose money. This is not just some calculation in a spreadsheet. It’s a real and present danger.

Sound portfolio management gives you a framework to continuously strengthen your financial foundation. It allows you to increase the risk you take in crypto and elsewhere.

Risk and reward - they’re two sides of the same coin. We add risk, our investments go up, we take profits that flow back to our foundation. Our foundation gets stronger, and we can take more risk…. Rinse and repeat until Valhalla.

Don’t buy the jet with your crypto gains. Buy your jet from the diversified foundation you’ve built after rebalancing your crypto profits.

Portfolio Management is the noun. Rebalancing is the verb.

The core action of portfolio management is rebalancing. I define rebalancing as the systematic process of isolating risk and extracting profit.

Here’s a simple example of rebalancing:

Let’s say you invest $100 in the traditional 60/40 portfolio of stocks and bonds. Stocks and bonds have different risk and reward profiles, and you want to maintain balance in your portfolio between these two risk buckets.

One year, your stocks crush and jump from $60 to $100. Your bonds do well too, but not as much, ending the year at $50.

Now, your 60/40 portfolio is out of whack. Stocks are 66% and bonds are 33%. You need to rebalance. So you sell $10 of stocks (take profit) and use that cash to buy bonds. After rebalancing, you have $90 in stocks and $60 in bonds, back to the 60/40 balance you desire.

Crypto makes rebalancing more important, not less.

Crypto prices are more volatile than anything else in your portfolio. Prices change fast, which is great when they’re exploding higher but horrifying when they drop 90% in a weekend.

It takes discipline. You need to be ready. You need a plan.

It’s time to assemble… $BILLY

— Jonzzy (@jonzzyTV)

2:16 PM • Jul 11, 2024

Step 1: Define your allocations across the whole portfolio

The first step to setup your portfolio management system is to step back and review your big picture.

Start with your major asset classes, categories, and strategies — cash, stocks, bonds, real estate, crypto, etc. We’ll worry about individual stocks or tokens later. For now, we’re thinking about the forest, not the trees.

Here’s an example portfolio:

Risk Level | Portfolio Target | Expected Yield | |

|---|---|---|---|

Money Market | Low | 10% | 4% |

Real Estate | Moderate | 40% | 10% |

Stocks/Bonds | Moderate | 40% | 10% |

Crypto | High | 10% | 50% |

With targets set, now all there is to do is rebalance periodically, exactly like the example above.

If crypto rips, that portfolio percentage will rise above target. That’s your sign to take profit and use the funds to rebalance to target.

You can trigger this rebalance based on time - every quarter, every year, etc. Or you could rebalance whenever an asset class gets 5%, 10% or 20% above or below target. Be mindful of transaction costs — it is possible to rebalance too frequently.

This mechanism does a few things for you.

It forces you to take profit, which can be very difficult when you’re feeling flush and greedy in a bull market.

It keeps your portfolio risk where you need it to be to protect your foundation. And,

It keeps you in the game – you don't sell your entire crypto portfolio, only the required amount to return to your target 10% allocation.

Isolate the risk, extract the gains. Protect your capital, and stay in the game.

What’s the right portfolio percentages for you?

I can’t tell you what the right portfolio allocations are for you - it’s too dependent on your unique financial and life situation. The right portfolio changes over time.

For example, my mother-in-law approached me last weekend and asked if she should buy some crypto. I told her absolutely not.

She’s in her 60s, retired, financially sound, and has no reason whatsoever to take on the risk that comes with crypto. Her crypto allocation should be 0% of her net worth.

For someone in middle age, maybe the right allocation is 1-5% of their net worth. For someone just getting started in their career maybe 10% or more could make sense.

Source: Bank of America Research

For a basic approach that’s simple and easy, I’m a huge fan of the Lazy Portfolios approach here.

For a more analytical approach you can customize for yourself (and one that’s well suited to crypto specifically), I go into deeper detail on how to think about crypto allocations in this post.

You can use my spreadsheet to get started, available here. You will still need to do the work for your own situation and plan accordingly.

Step 2: Define a target allocation for tokens and strategies within crypto.

Next, you should zoom in and run the same process on your crypto portfolio specifically. It's portfolio management all the way down.

You should do this for your other asset classes too – stocks, bonds, real estate, etc – but crypto is by far the most important. The volatility and emotional rollercoaster demands a systematic approach.

If you keep it simple and only own a single token or two, then step 1 may be all you need. Rebalance your crypto to your overall portfolio as needed, and sleep easy. Jack Bogle would be proud.

However, if you’re more active in crypto, holding many different tokens or if your bags are more than ~5% of your net worth, then I strongly recommend setting up a rebalancing system just for your crypto.

Set a target allocation for each token, basket, niche, or strategy as a percentage of your total crypto, and use those targets to systematically take profit on your winners, manage risk, and rebalance every month or so.

You could set up your allocations based on ecosystems (Solana, Ethereum, Base, Arbitrum, etc), sub-industries (DeFi, web3 gaming, memes, etc), or baskets based on narratives (AI, real world assets). The key is to identify concentrations and correlated assets, use those groupings to define your portfolio.

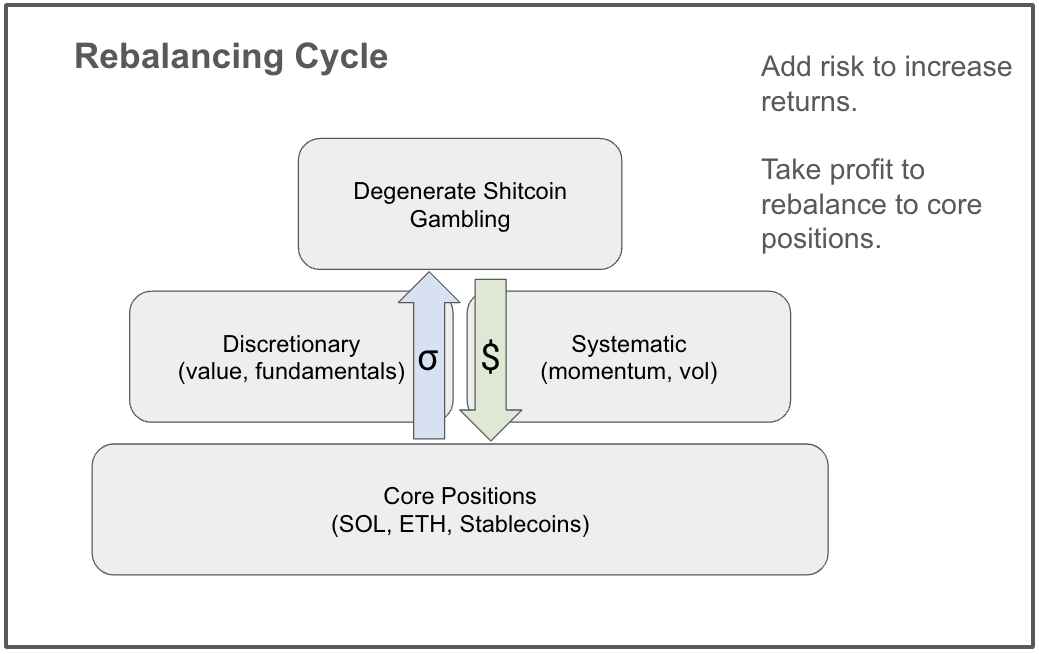

Here’s how I think about it in my crypto.

σ above is the greek letter sigma. Finance nerds use it to represent standard deviation of returns aka volatility.

I’ve mentioned in prior newsletters my differentiation between “Discretionary” and “Systematic” investments. Discretionary investments are based on my own logic and reasoning, while my Systematic investments are more quantitative, semi-automated, and based on momentum. I have a target allocation between those two sub-portfolios, my core positions in SOL and ETH, and some wiggle room to take on maximum risk in memes and ponzi’s.

I manage my Discretionary sub-portfolio manually, tactically investing across a few dimensions. I manage it based on concentrations across ecosystems (Solana, Ethereum, Bitcoin, Cosmos, Layer 2’s) and category (DeFi, currencies, Layer 1’s, Layer 2’s, Ponzi’s, Infrastructure, and Gaming).

Periodically I will run the entire portfolio through the volatility targeting portfolio system linked above, identify positions that are out of line, and adjust accordingly. I gave an example of how to do this in the RWA investment basket from last week’s newsletter.

My discipline isn’t perfect, but this strategy gives me the framework to be consistent and intentional in my portfolio. A big focus for me over the rest of this year is to increase the automation in my portfolio management – less emotion, more systems.

Step 3: Cash is King

The final pillar to any and every crypto portfolio is cash.

Cash is the only asset accepted by the IRS, which is important for things like not going to jail for tax evasion.

Also, cash can be readily converted into NetJets memberships and first-class upgrades. Not bad.

Move to cash before portfoliogone

On the other hand, cash kinda sucks in inflationary environments, so make sure your cash is earning a quality yield, 4%+ APY in today’s market.

When holding cash as part of your crypto allocation, keep it on-chain in stablecoins like USDC or DAI to save on transaction fees (moving crypto back to USD off-chain can be very expensive if done haphazard).

Plus, stablecoins can earn well above market yields on-chain than even the best savings or money market account.

I’ll write more on this in the future, but here’s a primer I wrote last month for more on yield farming DeFi.

Right now my cash holdings in crypto are relatively low, with most of my crypto portfolio deployed into my various token holdings (cough ETFs for bitcoin and ethereum are here cough bitcoin halving was less than 3 months ago cough).

However, as the cycle moves forward, I will have a significant sub-portfolio of cash in DeFi earning yield.

When you take profit, focus on your portfolio

So what should you do with all that cash after you sell your big winners?

You should rebalance.

Stick to your system. Isolate your risk and extract your profit. Stay in the game

And don’t forget to pay your taxes.

Portfolio Update

After a brutal weekend for crypto prices, I did not make any trades this week.

Market Vibes