- Positive Skew

- Posts

- 6 tokens for crypto's hottest narrative

6 tokens for crypto's hottest narrative

Don't buy one. Buy the basket.

Jay Jenkins

July 07, 2024

The hottest narrative in crypto right now is “real world assets.”

WTF is a “real world asset”? Leave it to the crypto nerds to come up with the worst names ever. This is why we can’t have nice things.

Real world assets (RWAs) just mean asset classes that already have markets in traditional finance. Real estate. Mortgage backed securities. US Treasuries. Corporate bonds.

In this newsletter I’ll explain why you should care about the RWA narrative and give you a basket of six tokens well positioned for the trend.

And instead of recommending just one or two as my top picks, we are going to take a diversified approach and build a portfolio with all six based on market correlation, volatility, and their fundamentals.

Why should you care about “real world assets”?

If “real world assets” already exist in traditional finance, what’s the angle for us as degenerate crypto speculatooors?

Many, if not all, of these assets could be originated, securitized, and/or traded more efficiently on crypto rails. Wall Street can make more profit and offer a better product to their clients, and we can invest in these tokens to meet them there. Win-Win-Win.

The opportunity is huge. Boston Consulting Group projects a $16 trillion tokenization market by 2030.

The total addressable market for tokenization is much larger still. There are $11 trillion in outstanding mortgage backed securities today. Over $300 billion worth trade daily.

The U.S. Treasuries market is even larger than that — $27 trillion outstanding and nearly $900 billion traded every day.

Thats $38 trillion right there, and we are just getting started: commercial real estate, derivatives, corporate debt, equities, stablecoins, and on and on…. the true market opportunity could be over a hundred trillion (or more).

Who are the top RWA players in crypto today?

I’ve chosen 6 of the largest and most reputable projects in the crypto RWA space for this basket.

First, I’ll give a very brief overview of each – what they do, how each token works, and recent market action. Then we’ll pull them together into a basket that can be invested together to capture the RWA upside.

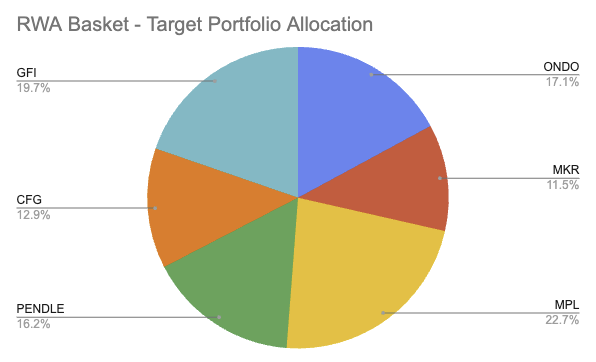

For each token I include a number from 0 to 20 as my price forecast. 20 is maximum bullish, 10 is market bullish, zero is neutral (so no allocation). This scaling is done to match the design of the portfolio allocation model we’ll use at the end to position these into a basket.

ONDO | MKR | MPL | PENDLE | CFG | GFI | |

|---|---|---|---|---|---|---|

Market Cap | $1.4 billion | $2.1 billion | $95 million | $575 million | $200 million | $170 million |

MC All Time High | $2.1 billion (2024) | $5 billion (2021) | $300 million (2022) | $1 billion (2024) | $475 million (2024) | $400 million (2024) |

1-Year Change | n/a | +129% | +98% | +310% | +17% | +401% |

Basket Allocation | 17.1% | 11.5% | 22.7% | 16.2% | 12.9% | 19.7% |

ONDO

Ondo is a platform that gives institutions the ability to tokenize traditional financial products (like US Treasuries), bridging TradFi with DeFi. Ondo provides technology and frameworks that ensure compliance with regulations like Know-Your-Customer and others so that TradFi firms can bring securities on-chain in compliance with all the regulations that apply.

Ondo makes money on the yields from the RWAs held on the platform. This is a similar business model to the world’s largest stablecoin issuer, Tether (Ondo’s stablecoin is USDY and includes a yield, which Tether’s USDT does not!). Tether, for context, earned $4.5 billion in profit…in just the last 3 months.

The business model is fantastic, but the ONDO token leaves a lot to be desired. The token gives you governance voting rights in a small subset of what Ondo does (it’s lending protocol, FLUX). There is no link between Ondo’s cash flows and the ONDO token.

So even if Ondo makes $4.5 billion in one quarter, none of that cash flow accrues to token holders in any way, shape, or form. (Blame the SEC for this — or maybe thank them? Is this the “investor protection” we’re paying our taxes for?)

The token’s market cap is only 14% of it’s FDV. Most of the remaining tokens are reserved for ecosystem incentives, but still, that’s a lot of new tokens just waiting to dump on you. The next major token unlock will occur in January 2025.

Ondo’s price action has been quite strong this year, with excellent momentum characteristics. It’s benefiting from the RWA narrative across the board, and particularly so after they were selected to power Blackrock’s BUIDL tokenized yield product and several other notable on-chain products from existing TradFi players.

Conclusion: Trade it, but get out before the January 2025 token unlock. Ondo is winning the Wall Street book right now, and that’s going to create a lot of upside. I give it my default market bullish rating of 10 only because the tokenomics are so bad.

MAKER

Maker was early among large DeFi protocols to embrace RWA as collateral, and today around 80% of protocol revenue comes from off-chain yields.

Maker offers a US dollar stablecoin, called DAI, and a governance token, MKR, that you can buy for the right to vote in Maker’s operations.

Maker allows users to deposit collateral and then use that collateral to borrow DAI.

Maker has a complex tokenomic model. MKR can be burned based on protocol revenue, while other times new MKR is created to cover any collateral shortfalls in the system. On net the MKR supply is stable, but it is market dependent.

95% of MKR tokens are in circulation. No issues with low float, high FDV here.

MKR has had weak price action for several years. There’s not much momentum to speak of and it underperformed the market yet again during this years bull run.

Conclusion: Maker is a rock solid protocol and great business, but it’s hard to imagine a 100x from here. I give it a 5, bullish but market underperform.

MAPLE

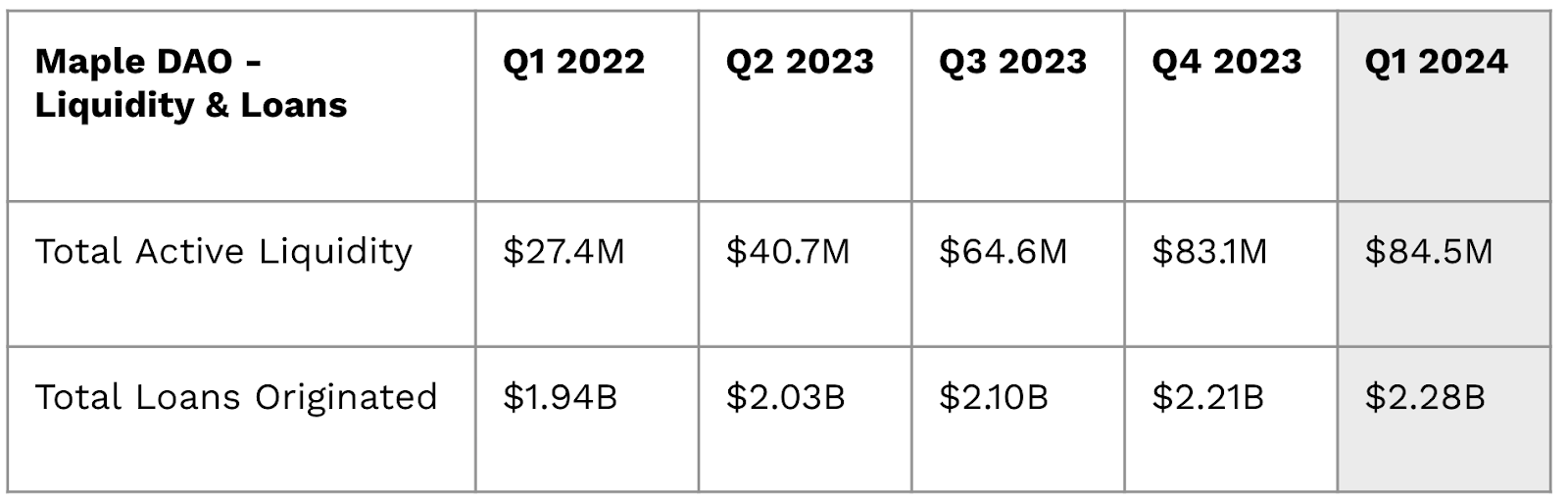

Maple is a lending protocol for onchain entities and the smallest market cap of the six covered here. It offers fixed yields as well as undercollateralized loans. Maple originates around $2 billion in loans per quarter with steady growth over the past year.

The Maple token, MPL, gives you voting rights in governance in the Maple DAO. In addition to governance rights, the MPL token can be staked to earn a share of the fees generated by Maple. Further, MPL holders can vote to provide additional liquidity to their preferred liquidity pools on the platform, further increasing yields.

The MPL token has a capped supply and 78% has already unlocked. It’s traded in line with other RWA tokens so far this year.

Conclusion: MPL is priced cheap compared to its strong loan volumes. It has a low market cap today, which is an appealing feature for crypto buyers who want maximum upside.

For the more traditional minded, the token has a strong, direct connection to Maple’s cash flow from operations, and the business model overlaps with the tokenization/RWA narrative very well. I give it a 15, bullish and market outperform.

PENDLE

Pendle captured lots of attention this cycle, ripping from $0.04 to $7.50 over the past 2 years. Bear market? What bear market?. That’s a 188x return and it’s still less than half the market cap of Ondo and Maker.

Pendle functions like an interest rate derivatives platform, collecting fees from users who buy, sell, and trade yield. This is hugely popular with crypto traders - at its peak last month Pendle had over $6 billion locked in the app. (that number is down quite a bit this month for reasons related to Yield Farming from a handful of large incentives programs and out of scope for the newsletter this week).

It’s benefited more recently from the RWA narrative – Pendle is integrated to Maker’s RWA pools and offers derivatives on top of those products. This integration allows Pendle to leverage Maker’s established ecosystem, providing a stable foundation and user base for its derivative products.

Pendle unlocks over time. Steady but not crazy.

The PENDLE token has a fixed supply and approximately 60% of the tokens are already unlocked. There are no further large token unlocks, only steady new tokens entering the market. This pressure is of concern, but thus far momentum has been quite strong and easily overpowered that sell pressure.

Conclusion: Pendle's complex product offering, strong adoption, compelling narrative, and good tokenomics make it a strong play in the RWA space. While its fully diluted valuation (FDV) has seen a significant run-up, there is potential for continued growth given its integration with major players and the ongoing interest in RWAs. I give it a 12, bullish with a watchful eye on further adoption.

CENTRIFUGE

Centrifuge is a layer-1 blockchain designed specifically to support the tokenization of RWAs. Unlike Ondo, Centrifuge does not offer their own products, only infrastructure that can be used by others.

The protocol supports tokenization of asset-backed securities and structured products, which provide investors with exposure to RWAs on-chain. This is classic Wall Street tech, but on-chain.

Centrifuge's native token, CFG, is used as gas for transactions (like ether on Ethereum or SOL on Solana), which means that increased protocol activity translates directly into higher demand for the token.

Tokenomics for Centrifuge are inflationary, with most tokens used as rewards for participation on the network. Approximately 90% of the tokens have already been unlocked, reducing the risk of significant future dilution.

Centrifuge’s price action has been similar to the broader market – not much beta here. It does benefit directly in the RWA narrative, though it is currently overshadowed by players like Ondo.

Conclusion: Centrifuge may not have the same market/narrative presence as some of the other tokens, but it’s a credible player in a corner of the market that’s hot right now and has huge upside. I give it a 10, market bullish, as I am cautiously optimistic given the huge addressable market.

GOLDFINCH

Goldfinch is like a traditional commercial lender that uses blockchain to improve its ability to access capital for it’s borrowers.

Goldfinch, like Maple, enables under-collateralized lending, but also allows for traditional “real world” collateral. This approach opens the door to using off-chain assets as collateral on-chain.

The protocol operates with a governance token, GFI, used to reward participation in the system for key roles like auditors and liquidity providers. Remember that Goldfinch is like a traditional commercial bank – it uses these GFI incentives to hire and retain the key functions it needs for the off-chain parts of its business - credit underwriting, audit, loan servicing, etc.

While the token supply is fixed, Goldfinch has the power to change the tokenomics by a vote of GFI holders if there is a desire to provide additional rewards/incentives.

68% of GFI tokens are unlocked and the majority of the remaining tokens are reserved for participant rewards. This reduces the likelihood of a large-scale token dump.

Momentum-wise, Goldfinch has been relatively quiet with a below-the-radar market cap and limited mainstream attention. However, its unique positioning in the under-collateralized RWA lending space is a nice counterposition to the others in the market.

Conclusion: Goldfinch's focus on under-collateralized lending and its ability to integrate off-chain assets into the crypto ecosystem make it a compelling project. The token has shown good beta in recent months, but remains our of major discussions. I rate it a 10.

Building the basket

It’s impossible to say which (or any) of these picks will end up doing the best. In situations like these with a broad opportunity and several projects competing, the right strategy is to allocate some capital to them all, taking into account their fundamentals, how correlated they are, and their volatility/risk.

I built this particular portfolio allocation using my preferred volatility targeting framework for crypto portfolios.

You can view the spreadsheet here to see the calculations. If you want to make changes, click “File”, then “Make a Copy.”

Let’s run thru a short example to show you how to build your own portfolio from this basket and allocation.

First, determine how much capital you want to invest in the on-chain RWA basket. In our example, we’ll say $1,000.

Then multiply your capital by each token’s Basket Allocation percentage from the spreadsheet or the pie chart above. The resulting number is how much cash you should put into each of the tokens to match this basket.

For the example $1,000 basket, you would invest:

Basket Allocation | Dollar Allocation | |

|---|---|---|

Ondo | 17.1% | $171 |

Maker | 11.5% | $115 |

Maple | 22.7% | $227 |

Pendle | 16.2% | $162 |

Centrifuge | 12.9% | $129 |

Goldfinch | 19.7% | $197 |

TOTAL | 100% | $1,000 |

Portfolio Update

The market has been all over the place this week, up and down but mostly down. It’s the usual crypto vol (hello Mt. Gox unlock) coupled with lower liquidity during the US holiday week and an increasingly bearish tone.

I took profit on the BILLY coin I bought last week. BILLY is up around 4x – I swapped my initial position back into SOL and intend to let the remainder run – Momentum remains strong, crypto twitter hasn’t fully picked up the meme yet, and that dog is just so cute.

Let it ride!!

Market Vibes

Billy is cute in any market… $BILLY

— Jonzzy (@jonzzyTV)

2:17 PM • Jul 5, 2024